29 Nov M&A Market Update through Q3-2016

IT and Healthcare deal activity down in 2016

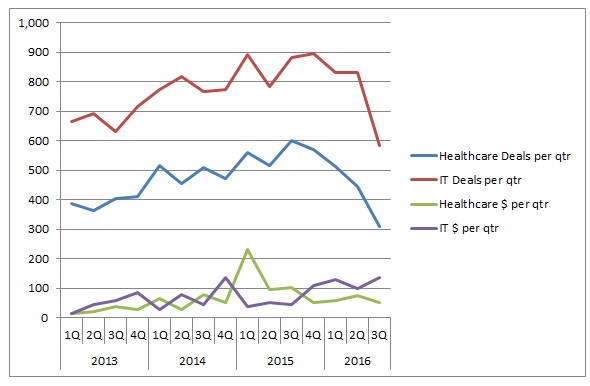

Now that we have M&A transaction data for three quarters of 2016 it’s clear that last year was truly a record year for global merger and acquisition activity. By contrast, this year the number of deals coming to market, across all industries, has fallen considerably. The slowdown has also affected the red hot sectors of healthcare and IT as the chart shows.

Completed transactions in IT and Healthcare by quarter

Here are some takeaways from the data through Q3-2016:

- Global M&A deal flow was down 25% for the first three quarters of 2016 compared to the same period in 2015. Despite the drop in the number of deals, the total value of M&A transactions (all industries) increased by 9.7% through Q3-2016 compared to Q3-2015. This reflects higher valuations and larger average deal sizes.

- The average valuation multiple for all transactions reached 9.4 times EBITDA, the highest level since the recession. For the same period in 2015 the average multiple was 8.8 times EBITDA .

- IT sector deal flow is down 12% in 2016 vs. 2015, yet the aggregate value of transactions is up almost 70%. This is due to a number of mega transactions such as EMC, Netsuite, and HP Enterprise Software.

- Software has dominated the IT deal space this year, followed by IT services. Software company multiples continue to increase while IT services and cloud/Internet multiples are stable.

- A majority of IT deals are driven by technology industry buyers, but there is increasing interest from non-technology companies and private equity investors.

- Healthcare deal flow has been dropping steadily since the third quarter of 2015.

- YTD healthcare transactions are off by 24.7% compared to the same period last year, and the cumulative value of transactions dropped by an amazing 57%, largely due to the huge dollar volume that occured in Q1-2015.

Sources: PitchBook, PWC, Ernst & Young